"Risk comes from not knowing what you are doing." - Warren BuffetIn Part I of my review I explored my initial conversation with Veritat Advisors. In this second part, I have decided to pay $250 for their initial financial assessment. I cover their Fact Finder, where you enter all of your financial data, and the Financial and Execution Plans, which are your advisor's advice for managing your money.

It's worth noting that Veritat has just announced that they are being bought by NestWise LLC, a subsidiary of LPL Financial Holdings Inc. There's not a lot of information available, yet, on what will change along with the ownership, but in a letter sent to customers today we were informed that service will continue and our financial advisor will remain the same.

A Man, A Plan, A Canal. Fact Finder.

|

| The Fact Finder. You'll spend plenty of time here shortly after you pay for Veritat. |

Done well, the Fact Finder will take a couple of hours to complete. During this time you will enter your savings account values, investment account holdings, spending habits, and answer other personal information about your financial life. It can be a bit tedious and I can't help but wonder whether the approach Personal Capital (or, to a lesser extent, Mint) takes might be a better way. Users give Personal Capital login authorization to view their accounts, so information about spending, savings and holdings are all automatically collected--and probably in a more accurate and detailed format than any user would ever enter on their own.* Something like this could make Veritat a one-stop-shop for both daily financial updates (checking credit card and checking statements) and long-term needs (investments and long-term goals.)

|

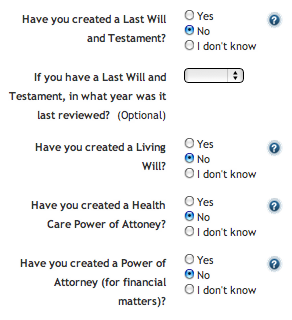

| See a glaring deficiency here? I didn't--until I completed the Fact Finder. |

Going through the Fact Finder, you may even figure out some of your deficiencies on your own. For me, the most glaring example was the estate planning section (screenshot to the left.) The one page where I had to enter that I've made no effort on a will or health care decisions was enough of a kick-in-the-pants to get me started on those tasks, even without waiting for the planner's advice.

After you've entered your personal and financial information you'll come to the Life Goals section. On my first run through the Fact Finder I set only one goal: the goal to buy a new home in the next few years.

Don't do that.

Instead, think about all of your financial goals and plans that take money and try to summarize them. Do you want to travel every year on a decent vacation? Include that. Do you want to buy a new car every 7 years? Include that. Do you want to save money for your children's college education? Include that, too.

When I first received my financial plan my money was used for buying a home and retirement. Nothing else. Only after realizing my mistake, and then going back and completing a more realistic assessment of my financial goals, did I get a financial plan that would actually work for me in the real world.

My mistake, though, led to one of the most favorable interactions I had with Veritat. It was my advisor who recommended that I add more goals. And my advisor re-did his work when I actually updated those goals. It's worth pointing out that, due to Veritat's pricing model, this did not cost me anything extra. I definitely came away favorably impressed, with the feeling that Veritat is working to set their clients up on a good and realistic path.

Planning and Execution

The payoff for all of your patience entering in financial information is the next two meetings you'll have with your advisor based on all your input. The meetings are centered around two documents, a Financial Plan which you'll receive shortly after your Fact Finder is submitted, and an Execution Plan, which you'll receive shortly after your discussion of the Financial Plan.

The financial plan starts with a dashboard and a summary of your goals. There's a lot of information in the document and, unfortunately, the document itself requires some explaining. That being said, all of my questions were answered on the call with my financial advisor.

Just below is a list of the sections of the feedback, along with a brief description of what is in the section and my thoughts on that section:

While reading the execution plan, before the execution meeting with my advisor, one of my disappointments in the execution plan was that I didn't feel like it was an easy document to work from. It contains a ton of helpful data, but it's a bit hard to pick out a list of tasks that I'll need to do in order to implement my plan.

But then, after the execution meeting, Veritat surprised me. On the website they gave me a list of tasks to complete, outlining everything I was supposed to do and allowing me to fill in the values that I actually used. Seriously, I think these checklists are great and, now that I know they exist, my plan is to use them to go through my tasks and the execution plan to figure out how I'm going to get it done.

*: The disadvantage in the Personal Capital/Mint approach is that you must give the sites your personal log-ins for your savings and investment accounts. While both the sites discuss their security and, I believe, have gone to great lengths to protect their user's data, the payoff for a rogue employee or successful hacker could be in the billions of dollars. That's a big target. And, even while I have been a happy user of Mint for over a year now, this does not set my mind at ease. Giving all of my banking credentials to yet another company is something I'd generally like to avoid. |

| Less red and more green is always good. |

Financial Plan Meeting

Just below is a list of the sections of the feedback, along with a brief description of what is in the section and my thoughts on that section:

Dashboard: A high-level overview of whether or not you are on track for your goals (see the screenshot to the right, as well as the one just above that.)

The Dashboard

Showing how much change is necessary,

and whether or not I can reach my goals.- Goal Summary: This is a list of all of your goals, when they will happen, the minimum and maximum dollar estimate you need to make the goal happen, your priority for the goal and the recommendations that come from your financial plan. When you get the financial plan it will be worthwhile to check and see that your goals are all there and adequately funded. I know that I looked at mine and realized that some priorities that I thought were High were actually Medium or Low, and vice-versa.

Lifetime Net Worth: This is a page showing a projection for how your investments and assets will appreciate over time. My advisor warned that it's not very accurate--meaning, I believe, that the year-by-year aspect of the projection could be very inaccurate, but if historical trends continue my investments might grow something akin to what is indicated.

Lifetime Net Worth: This is a page showing a projection for how your investments and assets will appreciate over time. My advisor warned that it's not very accurate--meaning, I believe, that the year-by-year aspect of the projection could be very inaccurate, but if historical trends continue my investments might grow something akin to what is indicated.- Budget: A high-level overview of your income, expenses and savings for the rest of the current year and the entire next year. Honestly, this page was just confusing to me--even after explanation I still struggle to understand it. Fortunately, it's an overview page, so it's not that important in the scheme of things.

- Recommended Saving and Debt Repayment: This is the first real page of substance in the financial plan. It contains your goals, how much of your current money you're going to allocate to them, how much you're going to save for them in the remainder of the current year, and how much you will save for them in the next year. The specifics of how you will do this and where you will put the money will be covered in the execution plan later. Right now we're just looking at how much and when.

Investment Portfolio: For each of your investment accounts there is a pie chart showing your current and recommended allocation of stocks and bonds. Your advisor will ask you what funds are available in your investment accounts and make recommendations based on those choices. That happens outside of the Planning and Execution documents.

The recommended change to my portfolio allocations.

I've been a very aggressive investor and it's probably

time for me to settle down a bit.- Investment Implementation: Like the Recommended Saving and Debt Repayment page, this page will show you how much to be saving in each investment account over the year, along with a more specific breakdown of the target portfolio (large cap, small cap, international, bond, cash.)

- Insurance Portfolio: Includes coverage recommendations for life insurance, accidental death & dismemberment, and long-term care insurance. My advisor stated that it's a start to the insurance conversation, but not the final picture. I am informed that the calculation used for life insurance is the Net Present Value (NPV) of that person's income along with debt repayment. For me, personally, this is too high as I don't want my wife to have too big a reason to put me out of her misery. For single income families and other situations this figure might be much more reasonable.

Estate & Will: A page dedicated to your eventual demise. Here you'll see the four documents Veritat thinks you should have and whether or not you should complete them. It's worth noting that Veritat also recommends companies you can use to complete the forms. And, since Veritat should not be making any money from these companies because they are fee-only planners, I am generally of the impression that they are decent companies at low cost.

I knew I had the wrong answers!

Execution Plan and Meeting

Once you and your financial planner have gone through and verified the financial plan, your advisor will have you schedule an execution plan meeting. Honestly this is the most exciting part: this is the document that will guide all of the changes you are about to make to your investments. Once again, I'll go through section-by-section:

- Risk Management: This section had helpful tips on how to set up insurance, estate, and will documents. Veritat recommended providers and gave specific information that you would need to insure yourself appropriately. This information should make it relatively easy and convenient to set up the documents with these services, though I think a truly prudent investor will do at least a quick search of competitors insurance rates, as well.

- Future Goals: This section summarizes your goal spending for the remainder of this year and all of next year, shows how much is allocated for that goal, and informs you which account the money will be taken from.

- Portfolio Action Plan: A summary, for this year and next, of saving, spending and transfers to and from each account.

- Transaction Plan: A list of money to save, money to transfer and rebalances to perform on each of your accounts over the course of this year and the next. This is the bulk of the execution plan.

- Portfolio Management: A reminder about Veritat's portfolio management service. I declined the service and, to their credit, never felt any pressure to join.

- Disclosures and Summaries: There's actually a lot of good information in the summaries of the companies that Veritat recommends here.

| One of my checklist tasks. |

Summary

And so I can truthfully report that I have been pleased with my initial experience with Veritat. I do feel like I've gotten my money's worth for my financial plan, both in direction and the efforts of my financial planner. I'm pleased enough that I'm planning to stay on as a monthly subscriber for at least another half year, to see if I continue to derive value from their service--although my plans may change as they merge and transition to NestWise. (Part IV of my review will discuss either the reason I left Veritat/NestWise during the transition or my impression on how worthwhile the $40/month service and quarterly meetings are if the transition goes smoothly.)

In Part III of my review I'll do a brief look at the advice I received from Veritat and how it compares to the do-it-yourself financial site bogleheads.org, but for the many of us who don't want to spend hours thinking about our finances, Veritat seems like a great way to go. If you've been considering using a financial advisor I would definitely try Veritat first. It won't cost you much, compared to an in-person advisor, and it might just cover everything you need.

The Good

- My financial advisor recommending that I add more goals, even though it made more work for him.

- The final checklist of actions I received from Veritat was top notch and will be useful for reporting what I actually did, since it might vary a bit from their recommendations.

- Throughout the experience I have learned a lot and feel like I am working towards a more secure financial future.

The Bad

- The Financial Plan and Execution Plan are difficult to interpret without assistance.

The Ugly

- The time spent gathering accounts and the initial data for the Financial Plan.

- The length of this post.

No comments:

Post a Comment